2. Economist- A person who study economics.

3. 2 branches of economics

a) Microeconomics- Study of a small part of the whole economy & deals with demand & supply of goods.

b) Macroeconomics- Study of the economy as a whole & deals with national income & international trade.

4. 2 statements

a) Positive statements- Statements of fact. It can be tested. E.g.: Brunei practices a mixed economic system.

b) Negative statements- Statements based on value judgement. It cannot be tested. E.g.: Inflation is a more serious problem than unemployment.

5. Scarcity- Excess of human wants over what can actually be produced.

6. Factor Of Production

a) Land - Reward is Rent.

b) Labour - Reward is Wage

c) Capital - Reward is Interest.

d) Entrepreneur- Person who organize the production & bears the risk involved. --> Reward is Profit.

7. Opportunity Costs- The next best alternatives that have to be foregone.

8. Free goods- A good in unlimited supply at zero price. E.g.: Sunlight.

9. Economic goods- A goods that involved price & in limited supply. E.g.: Plasma TV.

10.Public goods- A goods that can be used by everyone. E.g.: Streetlights.

11. Private goods- A goods that are priced & excludable. E.g.: Foods.

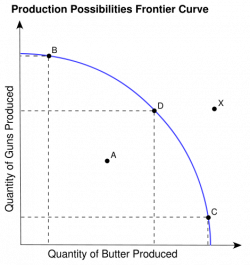

12. Production Possibility Curve- A diagram that shows the various possible combination between two goods that a country is capable of producing with given resources & level of technology.

13. Diagram of Production Possibility Curve

Economics in One Lesson: The Shortest and Surest Way to Understand Basi… - Amazon.com

14. Market Economy- An economy where markets are used to allocate resources through demand and supply and the price mechanism. No government intervention.

15. Planned Economy- An economy system in which the government manages the economy.

16. Mixed Economy- An economy system where some resources are owned by both private individuals and some by the government.

17. Assumption made about the market economy

a) Producers are driven by the profit motive.

b) Consumers get the best value of money when making purchases.

c) Consumers decide the types of goods to be produced.

d) Workers want to maximise their wages.

e) There is mobility of factors of production.

18. Advantages of the market economy

a) Producers will invest more in research & development due to high competition in markets.

b) No government intervention. Prices is determined by the forces of demand & supply.

c) Producers increase their productivity to maximise profits.

d) Higher rate of capital formation.

e) Faster response to market conditions.

19. Disadvantages of the market economy

a) Wasteful competition.

b) Limited competition between firms.

c) Unequal income distribution. Rich gets richer. Poor gets poorer.

d) Economic instability due to natural disasters.

e) Problem of external costs such as pollution.

20. External costs- A production costs borne by other people. E.g.: Pollution.

21. Assumption made about the planned economy

a) Consumers have to accept whatever goods & services offered by the government.

b) There is restricted mobility of factors of production.

22. Advantages of the planned economy

a) Government stabilize the prices so it would not fluctuate.

b) Less unemployment. Government can create job opportunities for new labour.

c) Possible rapid economic growth.

d) Greater income equality.

e) Welfare of the society.

23. Disadvantages of the planned economy

a) Lack of research & development.

b) Lack of choices for consumers.

c) Increase in productivity does not lead to an increase in wages.

d) Possible low economic growth.

e) Goods not required by the people are produced such as military equipment.

24. Mixed economy- An economy in which some production is done by the private sector and some by the state-owned enterprise or government. Resources are allocated efficiently with market forces at work. If the price mechanism fails, the government will then intervene to rectify the mechanism failure.

25. Why market failure in mixed economy?

a) Lack of public goods.

b) The presence of a monopoly.

c) The presence of external costs such as pollution.

d) Income inequality.

e) Lack of information.

Economics: A Self-Teaching Guide - Amazon.com

No comments:

Post a Comment